The decline of European banks over the last decade has been amply demonstrated. According to Petrofin Bank Research ©, the share of European banks as a percentage of the top 40 global shipping banks fell from 81.6% in 2011 to 61% in 2015 Notable examples of banks withdrawing or drastically reducing their exposure in shipping are RBS, HSH Bank and Commertzbank. There have been some notable exceptions, such as DVB, ABN, Credit Suisse and ING, who have expanded their exposure over the years.

The main reasons underlying the reduced European bank ship lending appetite have been: 1) capital constraints (Basel IV), 2) increased ECB regulation and monitoring, 3) high loan losses and provisions, 4) change of policy, to de-risk their portfolios and 5) inability to raise fresh capital, leading to deleveraging.

The main beneficiaries of the above contraction have been the following:

a) Chinese and Asia based banks

Possessing a higher deposit to loan ratio and with a greater ability to raise capital in a fast growing economic environment, these banks have managed to offset some of the missing credit capacity. Often linked to local newbuilding orders, these banks have focused primarily on publicly owned and large private shipping groups.

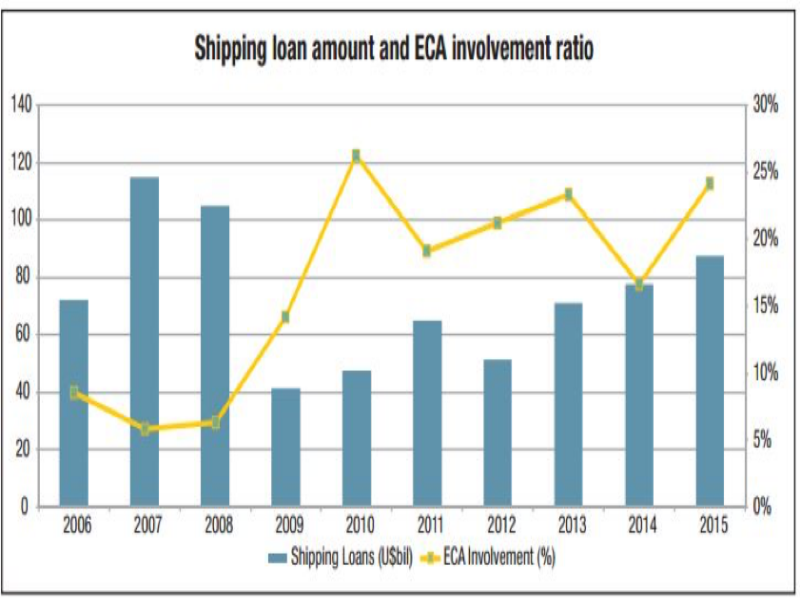

b) Export credit institutions

Export credit insurance assisted finance has developed fast over the years, offsetting some of the Western banks’ decline of capacity. Centred in China and Korea (CEXIM, KEXIM), they have developed as a leading newbuilding finance source. There has also been export finance in Europe e.g. GIEK, Atradius, Hermes etc., in support, largely, of the offshore related local shipyards. Export Credit Agencies involvement in shipping loans has increased markedly since the beginning of the crisis.

Source: Marine Money – January 2017

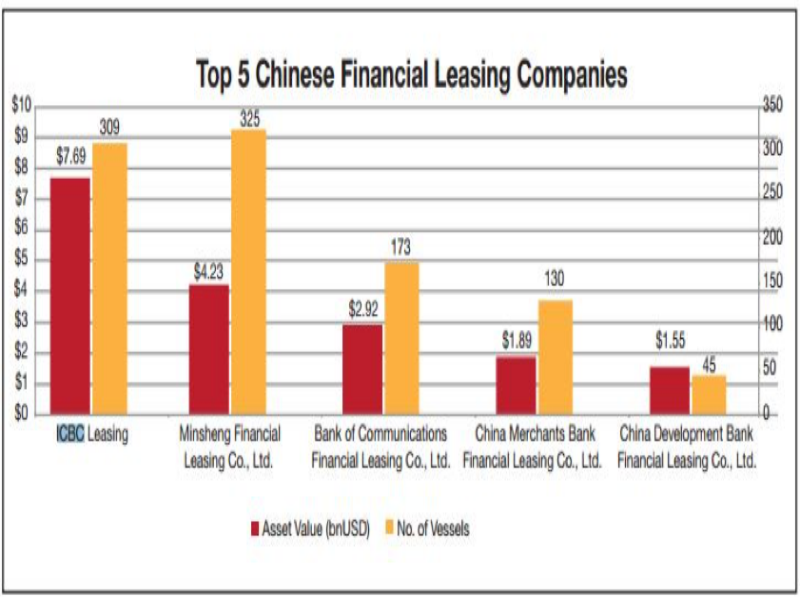

c) Chinese, Japanese and Korean leasing

The activity of leasing companies, often part of or associated with major banks, has increased. Examples include ICBC Leasing, Bank of Communication Financial Leasing, CMB Financial Leasing, Minsheng Financial Leasing and lately, Mitsubishi Leasing.

Source: Marine Money – January 2017

Far Eastern leasing companies have the advantage of less strict capital requirements than Western leasing companies and banks and can offer a more flexible approach both for newbuildings, as well as second-hand vessels, in their search for higher yields. Although still highly selective, smaller shipping companies have also been able to secure leasing finance.

d) Shadow banking providers or investment funds

The main development over the last decade has been by the various funds, which are unregulated and in search of very high returns. Increasingly, these have been developed not only in the US but also in London, Germany, the Middle East, Norway and Holland. They each have their own target markers and transactions and minimum IIRs.

With the adoption of Quantative Easing (QE) by the US and European central banks, deposit interest rates have fallen to near zero or even negative levels. In an effort to obtain positive yields, enormous quantities of funds, which were previously placed as deposits with banks, have switched into participating into such funds, whose growth has been explosive.

Fund managers, often, have a problem in the absorption of such funds and processing a sufficient number of transactions that meet their risk and yield criteria.

Some funds are opportunistic and seek returns of over 20% - 25% concentrating on higher risk opportunities and the purchase of bank loan portfolios at a discount. Some funds are investment only and seek to control the underlying investments, providing the vast majority of the required investment. Others consider a more sharing approach with their shipping clients and yet others only take up minority participations.

From the above, it is self-evident that unlike banks, each fund is geared to meet the specific investment targets and risks, as determined by their managements and accepted by their own investors.

Funds are competitive and wish to attract ever higher investment resources, so as to in many cases become market leaders. There are also purpose made funds often found in Norway, which are specific investment oriented, tailor made funds, promoted by specific brokers, such as Fearnley’s, Pareto and others.

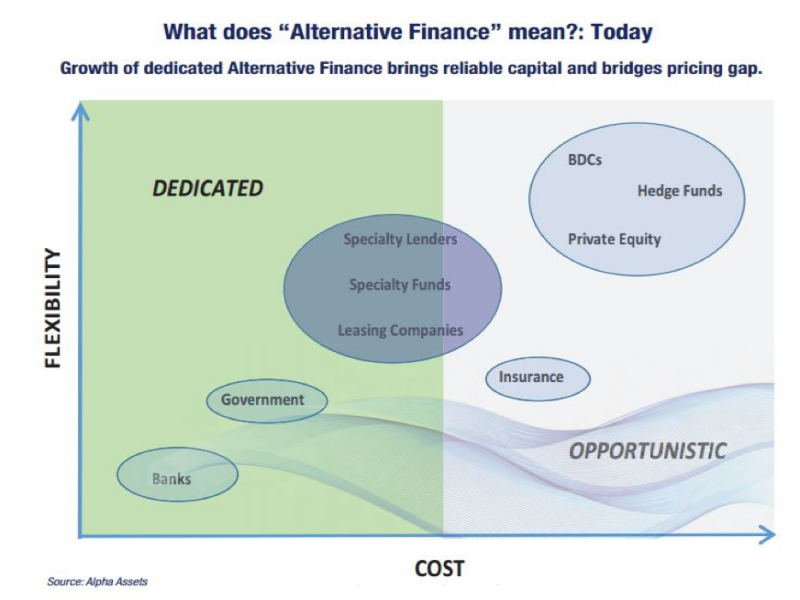

Lastly, recently, there have emerged quasi banking funds, whereby against lower banking style loan to asset values lending of 50% - 60% and often lower, they provide mirror banking style terms with, however, more flexibility as to the loan repayment profile. The returns sought by such quasi banking funds are in the order of 7% - 8% per annum, on a fully secured basis. These funds are taking advantage of the absence of bank interest into small and medium client transactions, which, however, are considered to be low-risk. Funds are generally more expensive and flexible than traditional bank finance. It is interesting to observe in the following table by Alpha Assets that each type of Alternative Finance occupies a different spot in the Flexibility / Cost relationship.

5) New banks

The bank finance vacuum has begun to attract the interest of new ship financing banks. Examples are the recently established M&M Bank in Norway, as well as the development of stronger interest by other banks, such as Berenberg, Warburg, Pareto Bank, Carnegie Bank and others.

Often, the margins required by such banks are to the order of 4-5% and higher, with loan to value loans of 30% - 50% being offered. Such is the appetite for shipping loans among smaller owners and projects deals that many such banks have already seen more demand than they can cope with.

Internationally, we have seen an increasing number of local banks throughout the world entering into shipping loans with local clients and this trend has also been in the ascendant.

Consequently, we have seen the ship finance gap that has been created by the reduction of Western banks’ appetite for shipping being replaced by the banks and institutions outlined above.

The last question that remains is whether Western banks might recover and return to shiplending in a similar style as in the past. The short answer is no, as the abundance of capital conditions, less stringent capital constraints and more lax regulatory environment are unlikely to return and are expected to instead increase.

There is a glimmer of hope, though, as shiplending margins and terms have increased and have begun to offer banks more meaningful returns for their capital. Should the outlook for both the European economy, as well as the financial markets improve, to the extent that banks will be able to increase their capital via stock market openings, it is possible that the period of bank consolidation over the past decade shall begin to stabilise and possibly reverse.

In addition, in the event that the unregulated parts of the banking and quasi banking industry, as well as investment funds shall become more regulated, it is possible that resources shall, once again, shift towards banks and deposits, especially in case interest rates shall rise.

A recovery of the shipping outlook for all market segments may also be the necessary catalyst to make shipping loans more attractive for banks, in relation to other forms of lending.

*Head Petrofin Research