As the Greek fleet is getting bigger and younger, it is also getting more consolidated.

The fleet percentage held by fleets of 25 vessels and over, in dwt terms, has risen from 42.27% in 2010 to 67.07% in 2017. Globally, vessels are also getting bigger in all market segments which is also the case for the Greek fleet, which is diversifying its trading patterns more and more. (Petrofin Research ©, published in March 2018 (www.petrofin.gr)

In order to finance the above developments in a shrinking bank finance climate, as has been demonstrated in the last few years, major changes have occurred.

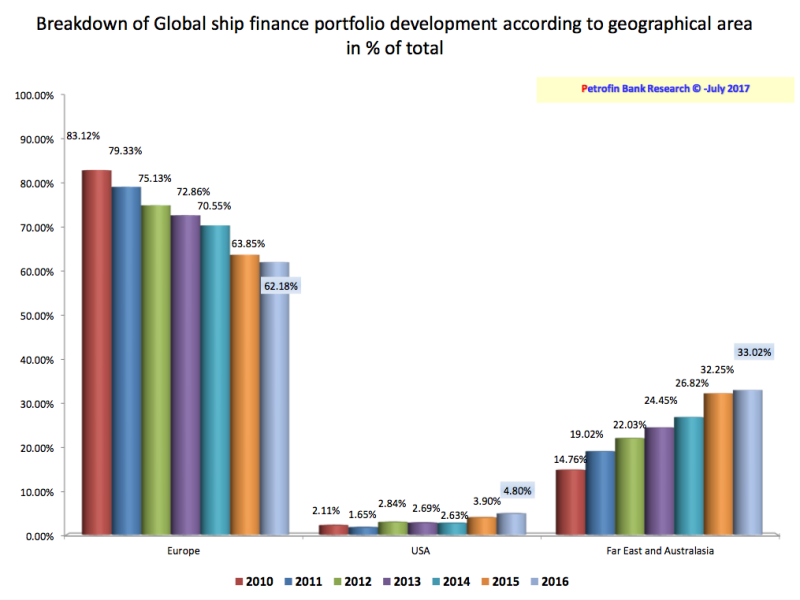

Although, traditional bank lending continues to play a leading role in Greek ship finance, Western banks in general and German banks in particular, in line with international ship finance trends, have declined both in market share, as well as in overall lending volumes. This reflects more their own financial and capital constraints rather than their attitude towards ship finance in general and Greek ship finance in particular. To a large extent, this withdrawal has been covered by Far Eastern banks and export credit agencies, notably Chinese and Korean. The global trend has continued unabated over the past 7 years with European banks’ share falling from 83% to 62%, whilst Far Eastern banks’ share rising from 15% to 33% (see Graph).

Greek ship finance has been affected by this decline with levels falling from $63bn in 2015 to $57bn in 2016, despite the growth of the Greek fleet. In the midst of this fall, the top 4 Greek banks have managed to largely retain their share and current research, thus far, points to some banks increasing their portfolios in 2017, including some of the Greek banks (see table of Petrofin Bank Research preliminary results on the top Greek banks - the full results of the latest Greek ship finance research are expected later in May 2018):

| Greek banks | 2016 | 2017 | Development |

| Piraeus | 2730 | 2750 |

1% |

| National Bank | 2368 | 2427.6 | 3% |

| Alpha | 2190 | 2225 | 2% |

| Eurobank | 1227 | 1524 | 24% |

Eastern financing entities (Banking and Leasing, as well as Export finance) have stepped in to fill the gap. Their client target has always been the big owners and the exponential rise to their portfolios has all but strengthened this preference. The question, thus, arises, as to what happens with the renewal and development of the smaller fleets.

As mentioned above, there is an indication that Greek banks are now in a better position to support Greek shipping, having been through a lot of turmoil in view of the Greek crisis.

Latest stress tests for Greek banks have been satisfactory and this is supportive of their increasing involvement in Greek shipping. The Greek banks are in a good position to enjoy a full range of services with their Greek clients and they continue to regard highly the concept of building up relationship. Currently, smaller owners remain not a focus group, but this may well change. Greek banks continue to also focus on client deposits which assist their liquidity.

The overall decline in market share by traditional bank lending has been covered by a variety of non- bank financing sources, notably Chinese leasing, as well as private investment and financing funds which (at a higher cost) have been willing to support the Greek expansion. Export credit finance has also supported local shipbuilding in the Far East. Lately, Japanese and other leasing companies have entered the sector. Public markets have played a reduced role but this trend is likely to reverse with Norway also playing an interesting role. There have been signs of smaller local banks both in Europe and the Far East expanding their activities in view of higher margins and fees, as well as use of bank services. Overall, the 75 top Greek owners accounting for 80% of Greek shipping have enjoyed multiple ship financing options and their growth has not been affected by the decline of Western ship financing banks. Such exodus is largely coming to an end, as banks have achieved their desired exits or reductions, whilst Far Eastern lending and alternative finance continues to grow. The recovery of many shipping sectors is also assisting the process.

Shipping is and will remain a capital intensive industry and as Greek shipping continues its growth, Greek ship finance in all its forms is expected to show solid growth in the coming years.

*Head Petrofin Research ©