Ship finance activity has followed the volatility of the global economy, banking and shipping in 2020 and 2021.

Concerning 2020, it can be divided into two halves. The first half bore the brunt of the disruptiveness of the covid-19 pandemic, with a severe disruption of trade and the negative effects to the global economy of lock downs and travel restrictions. As global markets plummeted, banks braced themselves for the economic and trade uncertainties before them and the detrimental effects on shipping vessel values and cash flows. Under these circumstances, it is quite understandable that bank lending and leasing slowed down.

In the second half of 2020, we witnessed a recovery across most sectors and especially in the dry bulk sector. The wet sector was an exception, with rates peaking in the spring of 2020, only to collapse thereafter during the year. As trade stabilized and China showed a robust recovery and subsequent growth, confidence returned to owners, as well as banks.

Bank lending picked up substantially and most banks ended with similar loan portfolios to those before the pandemic. Leasing staged an even more dynamic recovery and recorded further growth.

Overall, the year ended with the top 40 banks lending marginally down from $294.4 billion to $286.9 billion, due, mainly, to the departure of DVB and Nord LB.

The Petrofin Index for Global Ship Finance fell from 64 to 62, indicating, though, some stabilisation.

Capital market activity in 2020 picked up substantially, mostly in shipping bonds new issues from $6.87 billion in 2019, to $24.79 billion in 2020. Shipping follow-ons, too, showed growth from $2.66 billion to $10.73 billion and there were some shipping IPOs, as market confidence returned (Clarkson’s statistics).

There was, also, a pick-up in S&P transactions and values. For example in dry bulk, ship sales and values rose from 535 ($5.25 billion) in 2019, to 790 ($6.77 billion), in 2020. In tankers, although the number of transactions fell year on year, from 380 transactions in 2019 to 365 in 2020, in terms of values, transactions went up from $6.56 billion to $8.57 billion over the respective periods. (Clarkson’s statistics).

Banks continued to focus onto the incoming regulations regarding lower emissions and how these might affect their loan portfolios, as well as client / project selection. Many lenders joined the Poseidon Principles and, in general, banks became aware of the changing outlook for shipping up to 2030 and 2050, when the industry would be due to show zero net emissions, as a stated objective. In terms of lending, “green lending” had not manifested itself in earnest, as most owners were (and still are) searching for the right technology and assessing its likely cost / benefit. In the absence of a new universally approved technical clean solution by manufacturers, the discussions were mainly theoretical. The first signs of eco vessels’ strong preference by owners and tier 3 newbuildings manifested itself and picked up, as the year progressed.

2021 and beyond

In 2021, the global economy, international trade and overall shipping market have staged a robust recovery and good growth.

In Container shipping, depending on size, earnings rose 5, 6 and 7 fold, as the rebound from locked to open economies and the massive liquidity, economic and credit support programs in the US and Europe and strong growth from China, bolstered a swift recovery and acute pressure on the logistics chain systems. Port congestion both at the loading and discharging ports added to the growing inefficiencies and contributed to the massive freight rate increase and substantial increase in vessel values.

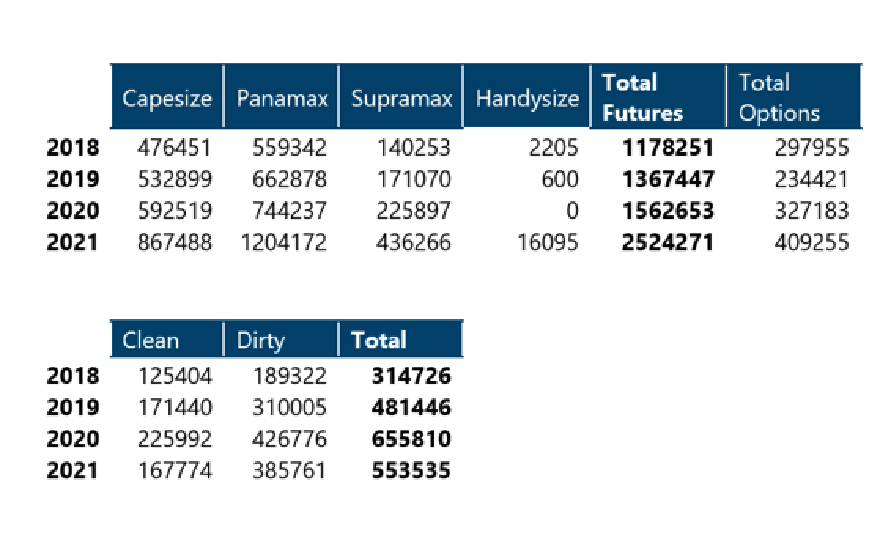

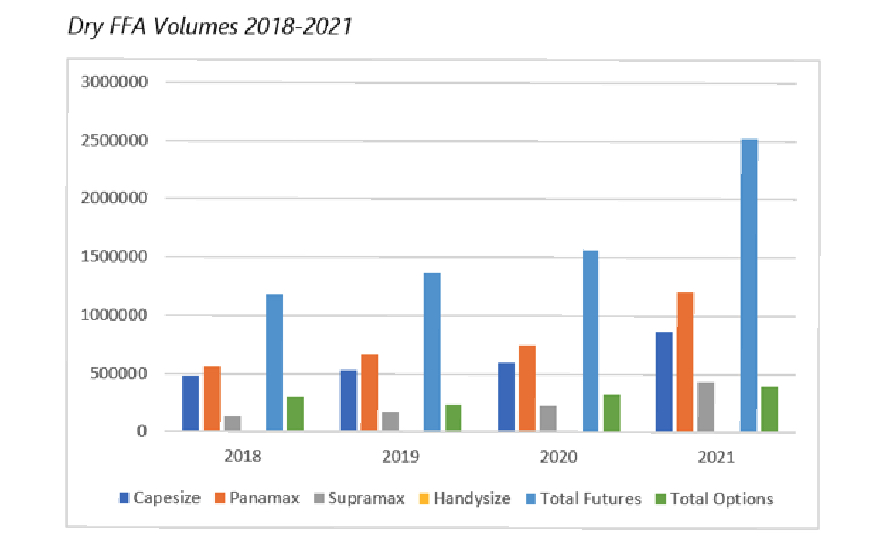

Not far behind, dry bulk shipping too, experienced similar congestion issues, in addition to the geopolitical results of the China – Australia commodity ban, coupled by solid growth by China and growth by all economic blocks. Charter rates grew approximately threefold from the start of the year and vessel prices approximately 80%, depending on size and age, with the ton mile requirements rising and a looming energy crisis fueling increased coal requirements by China and India. The demand for dry bulk appears strong and sustainable especially taking into account the relatively low growth of the fleet of about 3% in 2021, opposed to a much larger rise in ship ton miles demand. The effects of the pandemic are still restrictive and delaying vessel movements across all sectors, creating a shortage of vessels and pushing up freight rates.

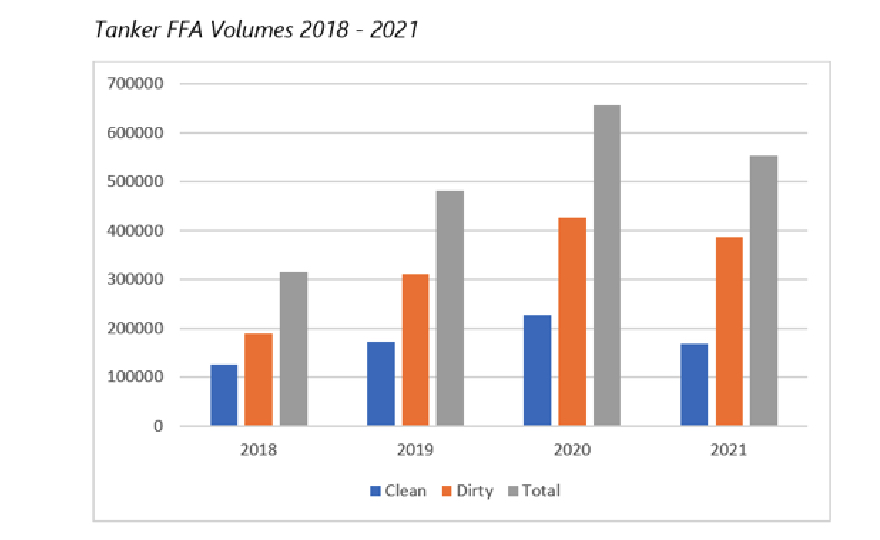

By comparison, tankers have shown a dramatic decline from the hefty spring 2020 rates, with all sizes recording big falls, especially in the dirty sector. Surprisingly, vessel prices have risen across all tanker types by 11% (Clarkson’s statistics), as many believe that sooner or later the wet sector will recover, supported by a higher demand for oil and oil products, as a less expensive fuel to LNG prices, which have risen multifold.

The other sectors, LPG and chemical, have not seen important changes, unlike LNG vessels and car carriers, which have started to rise substantially.

With most markets being strongly supportive, in term of vessel values and cash flows, banks’ confidence and willingness to lend grew. The same applies to leasing providers, as well as all providers of finance.

The rise in S&P transactions across all sectors, created financing opportunities. In addition, with vessel prices rising, the total S&P sales in 2021 are expected to grow by 77% to approximately $44 bn for all shipping segments. We need to point out that the actual value of new transactions would also rise, due to refinancings.

Admittedly, the larger banks continued to support their clienteles, which would invariably consist of Tier 1 owners. However, bank competition grew and in general, as client liquidity, cash flows and asset values rose substantially, this supported additional lending. For Tier 1 clients, margins and fees declined due to competition but lending percentages remained relatively low as banks sought to contain credit risk.

Small to medium clients also benefited from the improved confidence by banks that primarily focus on relationships with them. In order to mitigate risk and as period charters are so strong, most financings would involve some secure income flow and a front loaded accelerated repayment.

It is anticipated and the impression we are receiving is that bank lending is expected to grow in 2021. The same and arguably more applies to leasing, which has continued to provide attractive alternatives to bank finance.

The good shipping markets have woken up IPO appetite and an increased support for shipping by the capital markets across all sectors, also for follow-ons and shipping bonds, with 2021 totals expected to be similar to 2020 but with a much bigger number of transactions in the pipeline.

A new driver for lending and bonds is the sustainability linked loans and bonds. Driven by a wish to support cleaner, less emissions energy and ships aiming to meet environmental targets, an increasing number of banks joined the Poseidon Principles and started looking for green loans. By now, 27 banks have joined the Poseidon Principles and according to Citibank’s Michael Parker, amount to $185bn, in lending, or 64% of our top 40 global banks research. Examples of participants include leading Japanese banks SMBL, SMF&L, Shinshei, MUFG, Development Bank of Japan, as well as all the export finance entities, such as Atradius, Eksfin and others. European banks too have been looking for ‘green’ or ‘sustainability’ loans and some transactions have begun to surface.

According to the Institute of International Finance, in the last 18 months, there have been 30 – 35 sustainability loans.

The recent IDX / Intercargo global levy on carbon emissions proposal coupled by the EU’s own proposals awaiting EU Parliamentary approval has upped the pace on the risks / rewards / costs of meeting the emission standards. As most vessels are conventionally engined (non eco) vessels, meeting the new EEXI regulations will require either a significant ME derating with an associated loss of speed or expensive technical upgrading, retrofitting or other devices.

Complying with the new emissions requirements would entail a significant cost for conventional vessels. Moreover, as shipping is due to become a zero emissions industry by 2050, no one knows what technical solutions and fuel will be able to achieve this goal and at what cost. Owners and banks are bracing themselves for high capital expenditures, which will promote further consolidation in the industry and higher risks. It is also unclear what part of these additional costs will be borne by the owners, charterers or consumers and clearly, the stakes are high.

One benefit from the above uncertainties is that most owners are not rushing to massively order newbuildings, which has the desired effect of prolonging the good markets and adding liquidity for owners, which could be utilized to finance the ships of the future.

2021 is, therefore, expected to be a watershed year, in which global bank finance will end its long decline and should record a useful growth. The increase is expected both for the big, as well as the smaller banks, across the world.

In conclusion, shipping global bank lending is expected to rise in 2021 offsetting the downward trend over the last decade. The same is expected to apply for Greek ship finance as Greeks have been most active in Sale and Purchase transactions. According to Allied, Greeks have purchase 300 vessel for $2bn and have disposed of 183 ships for $2.54bn thus far. In addition, Greeks account for 11% of the new orderbook. It is self evident that Greek shipping is continuing its growth and will require the necessary lending. We anticipate that our annual Global and Greek ship finance research for year 2021 will reflect the above.

* Head, Petrofin Research©

S.A._small.jpg)