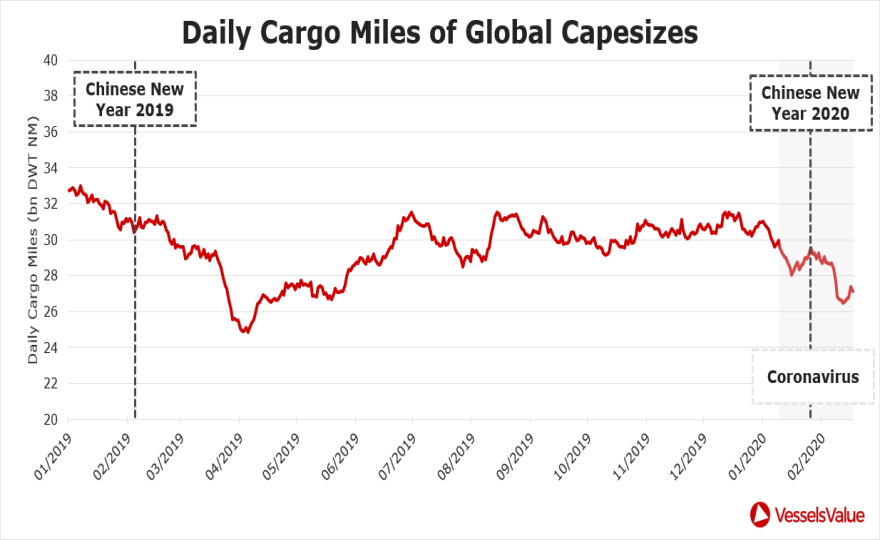

Observing ton miles for the Capesize fleet, data shows that whilst demand has dropped, it’s not as low as what we have observed in the past 12 months.

The 12-month low, related to last year’s Brazilian dam collapse, occurred on 5th April 2019 causing demand to bottom out at 24.84 bn DWT NM. Despite recent events, the measured demand across the sector has shown the first signs of recovery over the past few weeks:

Unsurprisingly, Chinese trades are continuing their downward trend due the compounded effects of the Chinese New Year and now Coronavirus:

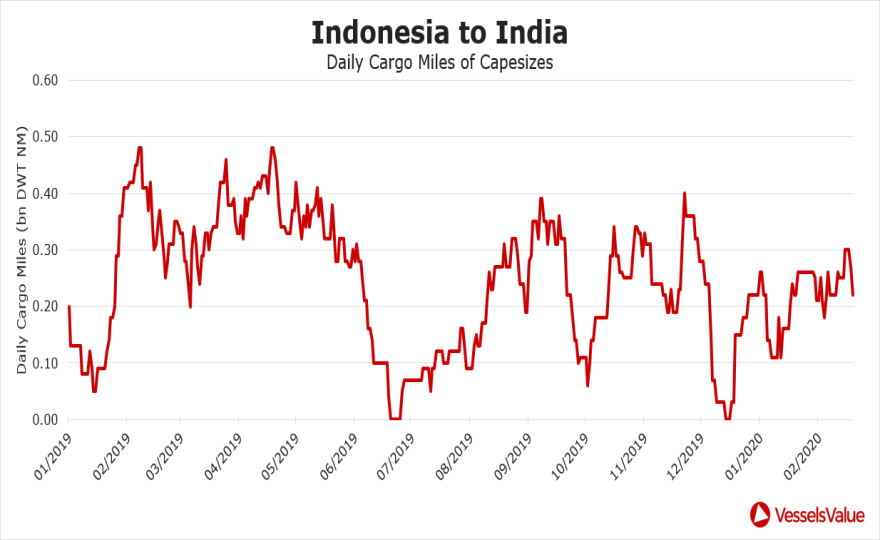

But other trade routes don’t appear to be suffering. For example, the Indonesia to India route (as shown below), whilst more volatile, has not shown a significant downward trend:

Japanese Demand

Recently, it has been announced that Japan’s largest iron ore importer, Nippon Steel, will be dramatically reducing their steel production. This reduction in Japanese iron ore demand could have further downward effects on the market.

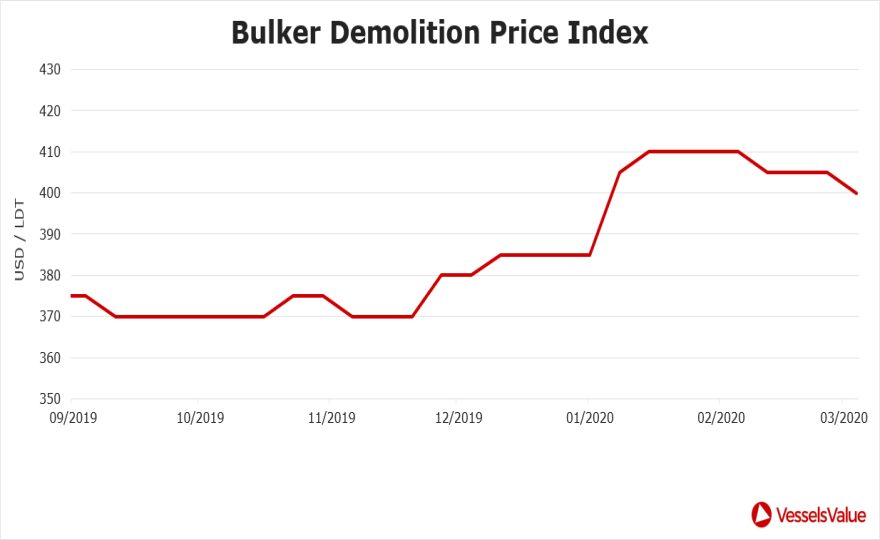

Vessel Recycling

Bulker scrapping rates have been increasing since Autumn 2019 which has already created a greater level of vessel recycling:

Comparing 2020 with 2019 (year to date), there have been 20 units sent for scrap this year vs 8 last year. In fact, only 27 units were scrapped throughout 2019 which means we’ve already reached over two thirds of this number whilst only being a sixth of the way through this year. The poor Bulk markets have been a factor in the increase of the number of vessels scrapped. The hope is that this increased vessel recycling will reduce fleet growth, possibly resulting in improved markets once ton mile demand bounces back.

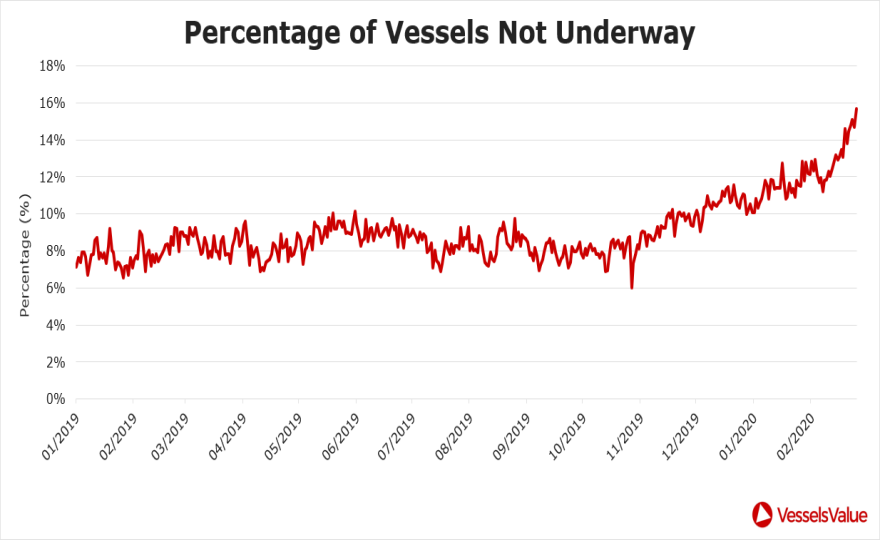

Utilisation

15% of the Capsize fleet is currently not underway (i.e. sailing), which is a good (but not perfect) indicator of fleet utilisation. This is almost double the 2019 daily average of 8.5% of the fleet not underway. This signals, unsurprisingly, the challenging state of the capsize market.

Summary

The Capesize market is heavily reliant on Chinese demand of iron ore. This is down significantly due to the economic effects of coronavirus. The result has been falling Capesize cargo miles, vessel utilisation and earnings. We hope that the effects are short lived and expect a bounce back, and possibly a positive catch up overcorrection once normality resumes. Japanese demand reduction is a further downside risk, while increase vessel recycling is positive for the market.

S.A._small.jpg)