The shipping industry is responsible for about 3% of Global Greenhouse Gas (GHG) emissions and faces increasing pressure to reduce its environmental impact and align with the Paris Agreement goals.

Decarbonisation in finance is one of the key strategies that finance providers are adopting to achieve this objective. It refers to the process of shifting financial support from carbon-intensive activities to low-carbon alternatives, such as using cleaner fuels, improving energy efficiency and adopting innovative technologies. In this article, we will explore how different stakeholders in both the banking and shipping sectors are involved in decarbonisation-oriented finance, what are the main challenges and opportunities they face and what are the best practices and examples of successful initiatives.

Who is involved in achieving the targets?

The main actors involved in decarbonisation finance are shipowners, banks, leasing companies, charterers, shippers. In addition, emission reduction product developers, class, flag, Rightship, consultants, insurance companies, and second party opinion providers (SPO). Each of these actors has a different role and motivation to participate in decarbonisation.

Shipowners are the primary drivers being the ones who own and operate the vessels that emit GHGs. They have a direct interest in reducing their fuel emissions in order to comply with regulations, meet the increasing demand for green finance as well as the customer demand for greener shipping (charterers, end-users) and further enhance their reputation. They can access various sources of financing to support their decarbonisation efforts,

such as green loans, green bonds, sustainability-linked loans, or blended finance.

Banks, leasing companies and alternative funds are the main providers of finance for shipowners and they have a significant influence on the decarbonisation agenda. They have a fiduciary duty to manage their risks and returns and they also have a social responsibility to contribute to the global climate goals. In order

to encourage and attract shipowners to adopt more sustainable practices, they use different mechanisms and incentives, such as offering lower interest rates, adjusting loan margins, providing higher LTV finance, increasing the amortization period setting, environmental criteria, or joining industry initiatives etc.

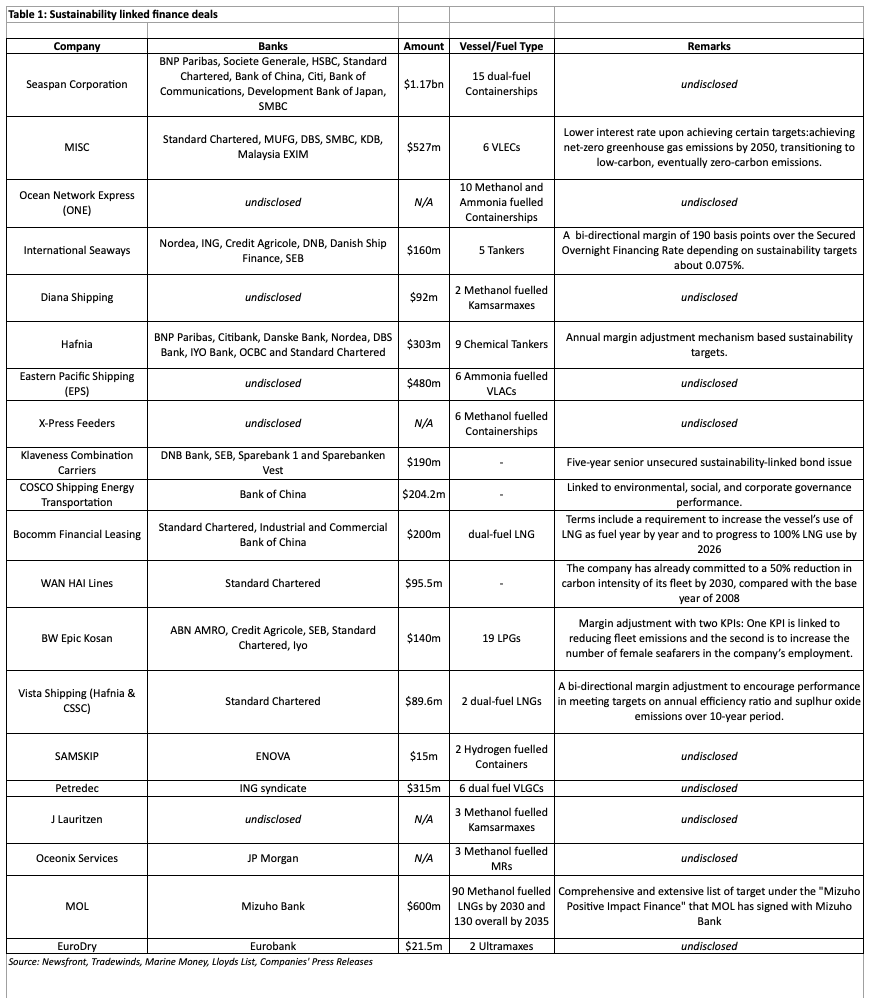

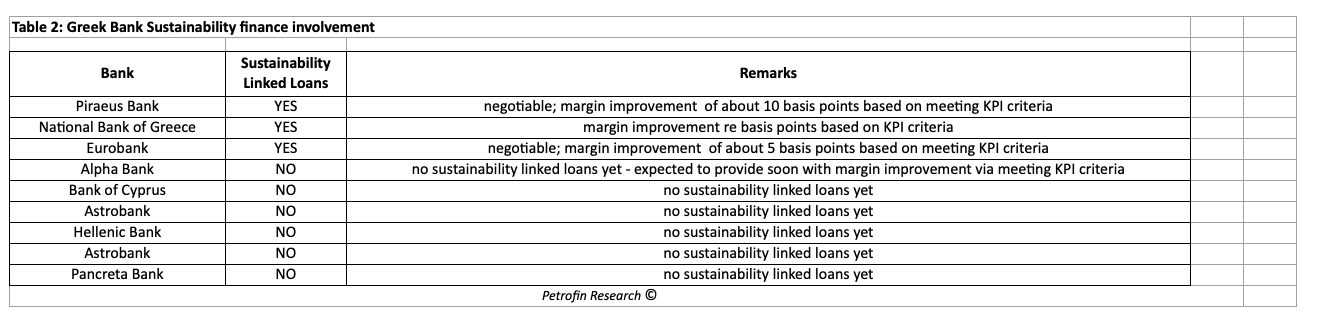

As more and more deals are being struck between banks and shipowners, we note the heavy involvement of Western and Eastern banks, particularly in syndications. As can be seen in the following table (Table 1), clusters of leading banks, such as BNP Paribas, Bank of China, Citibank, Danske Bank, Nordea, DBS Bank, IYO Bank, OCBC and Standard Chartered etc., act as lead arrangers, bookrunners, administrative agents, sustainability coordinators and other roles in the same deal. Interestingly, more and more Greek banks are involved in sustainability linked loans (Table 2). The three banks that held 67% of the Greek banks’ shipping portfolio (Piraeus, NBG and Eurobank) in 2022 (Petrofin Research©), are now already participating in sustainability linked loans.

It should be noted that leasing companies and other alternative finance providers are characterised by their higher LTV and flexibility offering more tailored solutions to shipowners who want to invest in new or retrofitted vessels that are more energy-efficient or use alternative fuels.

Moreover, another key stakeholder are the charterers whose preference for energy efficient ships is increasing. As a result, and considering the cost of such vessels, there are on-going discussions regarding the participation of charterers in the form of higher rates when utilising them in order to encourage such investments by shipowners. This is already reflected in the development of a two-tier market where eco dual-fuelled and other energy efficient vessels are preferred and provided with higher rates than conventional technology.

Noteworthy, that in the reported green finance deals, SPOs range from banks to classification societies and independent providers of eco-research and ratings (e.g Sustainanalytics) etc. Their involvement enhances the credibility and transparency of decarbonisation in finance by applying consistent methodologies and standards. They provide autonomous and objective assessments as well as recommendations of the environmental aspects of a financing instrument or project.

What are the main challenges and opportunities?

Decarbonisation in finance is not without challenges and barriers for the shipping industry. Some of the main challenges include:

• The complexity and diversity of the shipping industry, which requires a holistic and collaborative approach among various stakeholders with different interests and perspectives.

• The high cost and uncertainty of developing and deploying

new technologies and fuels that can achieve zero or low-carbon emissions. The use of bridging fuels facilitates the transition from conventional to new fuels. This is an interim solution, but the main challenge will occur when shipping will have to compete with other industries, such as cement etc., for the use of fuel technologies. Thus, it remains to be seen whether increased demand from other industries with a large need for new fuel technologies could probably lead to scarcity of these fuels in shipping.

• The difficulty of measuring and reporting the environmental performance and impact of different financing instruments or projects related to decarbonisation.

• The lack of standardised practices, clear and consistent regulations and policies that can create a level playing field and incentivise decarbonisation across the industry, despite the use of SPOs.

On the other hand, it is interesting to note that decarbonisation also offers many opportunities and benefits for the shipping industry. Some of the main opportunities include:

• The opportunity to gain a competitive edge and attract more customers and higher rates by demonstrating leadership and innovation in sustainability particularly for the big players.

• The potential to reduce operational costs and increase profitability by improving fuel efficiency and switching to alternative fuels.

• The possibility to access new sources of financing with much improved terms, especially loan margins, by meeting the environ- mental criteria or expectations of investors or lenders. There have been numerous green investment funds concentrating exclusively on green loans, i.e., lower emission vessels and / or alternative energy uses.

• The chance to contribute to the global climate goals and enhance the reputation and social license of the shipping industry.

What are the best practices and examples?

There are many examples of best practices and initiatives that showcase how decarbonisation in finance is being implemented and promoted in the shipping industry. Here are some of them:

• The Poseidon Principles provide a global framework that assesses how ship financing aligns with the global climate goals. The principles are based on four core commitments: assessment, accountability, enforcement and transparency. Thus, the banks that take part in this are required to measure and disclose the carbon intensity of their shipping portfolios as well as to work towards reducing it over time. There are currently 34 signatories jointly representing approximately $200bn in shipping finance and more and more banks are working towards joining this global framework (PoseidonPrinciples.org).

• The Sustainability Margin Adjustment Mechanism is a tool that links the interest rate of a loan to the environmental performance of the borrower (Loan Market Association – lma.eu.com). The mechanism allows for a margin adjustment (either positive or negative) based on predefined environmental indicators or targets, such as GHGs, energy efficiency, or alternative fuels. The mechanism creates an incentive for borrowers to improve their environ- mental performance and rewards them with lower financing costs. • Flexible finance terms are also adopted by banks and pro-

vide some flexibility to borrowers on how they use the funds, as long as they are used for sustainability purposes. The goal of

this mechanism allows borrowers to access funds for general corporate purposes but also to allocate funds for specific green

or social projects, as well as the main goal which is investing in new or retrofitted vessels that are more environmentally friendly. These enable borrowers to switch between different uses of funds depending on their needs and opportunities.

Main issues

As stated above, lower consumption and emissions achieved by shipowners come at a considerable cost. The two-tier market consisting of green vs. conventional vessels is not clear in terms of vessel income (hire rates). More specifically, it is not clear whether the incentive from end-users is there to justify and sup- port such investment, at least presently.

It is also difficult to assess the IRR of such green investments

in relation to each measure designed to reduce emissions, e.g. dual fuel, batteries, wind sails, retrofits, etc. The margins benefits appear to be modest in relation to the higher investment cost for lower emission, dual fuel vessels and other alternative technologies. The reward and penalty terms for shipowners are unclear and not standardised. In addition, as they vary according to use as well as geographical location and trading patterns, it is uncertain what responsibility will be undertaken by charterers. Evidently, what is required is a level playing field in which all stakeholders are aware of the costs, benefits, incentives, responsibilities and participation in the green transition.

Thus far, the banking industry has taken on board in a positive manner the regulations. Although it has the desire towards to contribute and reduce shipping’s environmental impact, the ‘economies’ for the shipowners are unclear.

In order to form a better idea of the current situation and challenges, more transparency is needed by all stakeholders. Although sustainability-linked terms are not often published, some public companies provide some information and thus far there is little information for private companies. This is expected to change

as more and more banks are coming forward with their terms encouraging shipowners towards decarbonisation.

Conclusion

Decarbonisation in the banking and shipping industries is being adopted to reduce the environmental impact of their respective operations and align with the global climate goals. Green finance involves shifting financial flows from carbon-intensive activities to low-carbon alternatives, such as using cleaner fuels, improving energy efficiency, and adopting innovative technologies.

The challenges and barriers posed for the shipping industry are many, such as the high cost and uncertainty of new technologies and fuels. Furthermore, the situation is also burdened by the lack of clear policies as well as the difficulty of measuring and reporting the environmental performance. The shipping industry is characterised by the sheer complexity and diversity, which renders quite difficult to standardise.

The opportunities and benefits that are offered by decarbonisation for the banking and shipping industries are gaining ground as there are prospects for increased profitability and reduction

in operational costs in the future. As talking about the future can be precarious, it should be noted that stakeholders are forming alliances and are cooperating towards resolving and overcoming the main issues and problems. Combining their respective know- hows all parties are hoping for a smoother transition towards decarbonisation. A good example of this is the Methane Abatement in Maritime Innovation Initiative, where industry players bring together their expertise to help abate methane emissions. Therefore, a cycle of encouraging each other is evident.

It is important to note that the financiers of this transition are already playing a major role by taking the initiative of allocating more and more of their shipping portfolios towards cleaner vessels.

* Head, Petrofin Research©