Readers are invited to view our latest Petrofin Research © at www.petrofin.gr.

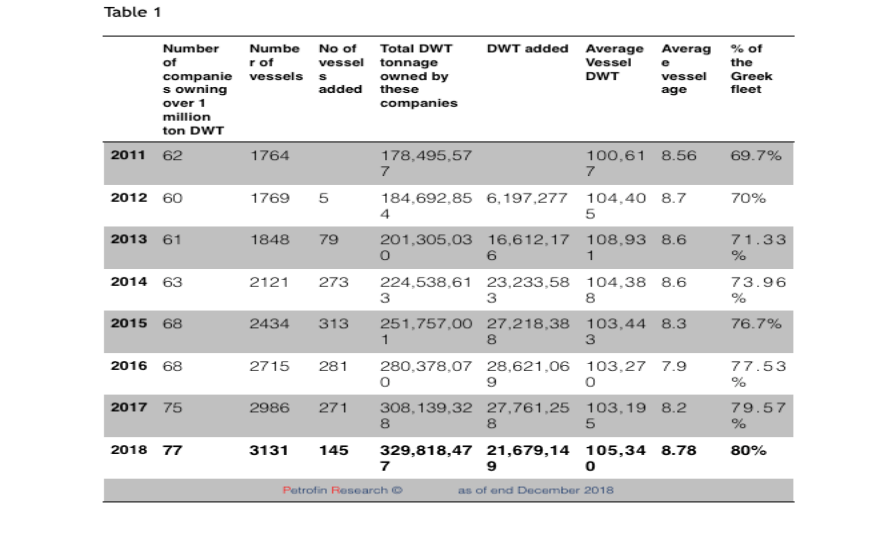

As a quick synopsis, the Greek owned fleet consists of 5,508 vessels of 412,310,405 DWT, accounts for 18.16% of the global shipping fleet and is run by 588 Greek companies. Due mainly to the economies of scale of larger fleets, the concentration levels have risen with only 77 companies now owning 80% of the Greek fleet. (Table 1)

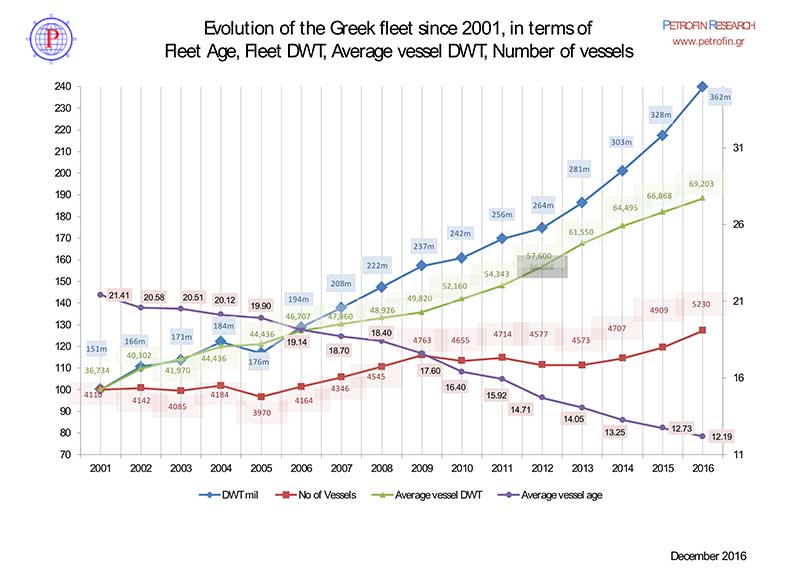

In Graph 1 you will find a very useful diagram with the evolution of the Greek fleet over the last 18 years in terms of DWT, number of vessels, average vessel DWT and age.

Can the growth and quality story of Greek shipping continue and what dangers lurk ahead?

To many, for a small country such as Greece to have the largest fleet in the world is a paradox. Greece, unlike China does not have a large economy to utilise a substantial part of its fleet. Greeks, therefore are international cross traders with their vessels rarely calling on Greek ports. Greece, again unlike China, does not have either a shipbuilding or a scrapping industry. Its local vessel servicing industry too is in decline as Greek vessels do not call in Greece and support services have to be provided in the far corners of the world. There does, however, still exist in Greece a network of engineering and technical servicing companies, which continue to compete internationally.

Greece used to rely more on Greek officers and crew but the growth of the fleet has not been matched by a growth of vessel going personnel. Greek seafaring training too is gradually being eroded as young people prefer shore based jobs despite the lure of higher wages offered by shipping. In this area, though, there is potential for improvement provided that Greek seafarers’ wages are in line with those of other seafarers of the same training and experience.

In the field of finance, Greek owners have invariably relied on non-Greek banks and finance providers to finance their vessels. Over the last decade, however, Western, and mainly German banks, have declined with a corresponding rise in the Far East finance and leasing. Greek banks, despite their internal problems related to bad loans and the state of Greek economy, have shown a remarkable willingness to continue financing Greek owners, as shipping represents one of the very few sectors with attractive risk/rewards. Nevertheless, Greek banks account for only 16.85% of Greek shipping bank lending (Petrofin Bank Research ©) and zero in respect of leasing, export finance or Private Equity funds financing. Greek owners, therefore, in the sphere of financing too are less supported than, say, their Chinese or Japanese counterparts.

The ever growing rise of regulations affects all owners. However, some nations discriminate in favour of their owners, which adversely affects Greeks as cross traders.

An area where Greek companies have enjoyed an advantage is that of experienced ex seagoing shipping staff. These highly qualified and capable managers have provided Greek owners with the technical and operational support they required to grow. As the Greek shipping sector’s requirements have grown and as the pool of such qualified personnel declines (on account of a decline in Greek seagoing officers), there is a danger that this relative advantage might also decline over time.

Due to higher costs, the lure of the Greek flag is declining which is unwelcome as it is on the basis of Greek flagged vessels that Greece has a powerful voice within the EU and other international fora.

In the fields of chartering and insurance, Greece has not developed its own capacity and the same applies to arbitration or the use of Greek law.

Taking into account all the above factors, one wonders how Greek shipping has succeeded so well as it has over the last decades.

The answer lies in the commitment and dedication of Greek owners who view shipping as area of excellence. The huge capital requirements of such Greek shipping growth are a testimony of their commitment, risk taking and ability to handle the requirements of their fleets.

Another area of relative advantage is on the timing of vessel purchases (including the placing of newbuilding orders and sales. This profit oriented investment strategy with an emphasis on capital gains has supported Greek owners in not only growing but also in disposing of vessels in a timely manner thus boosting their liquidity.

Responding to the question of whether Greek shipping competitiveness is being challenged by the above factors, some of which have turned negative, the answer is yes. Such challenge is not new and, thus far, Greek shipping has responded and raised its standards of maintenance, age and quality of its fleet, as well as organisation and practices. However, shipping as a highly fragmented industry does not have the power that its status as the 90% plus carrier of all commodities and products should provide. As such, shipping has become the target of hasty and one sided legislation plus the imposition of often contradicting rules and regulations, which have created uncertainty and higher trading risk.

Protectionism too is challenging Greek shipping as it encourages local owners and products at the exclusion of foreign goods and this generates less trade. The growth of state fleets or favoured local fleets has reduced the ‘free market’. As long as shipping demand outpaces such protectionism and affords shipping a viable growth, the free market demand should provide some comfort to Greek owners. The One Belt One Road Chinese inspired network could provide, however, a much needed impetus to international trade.

Without doubt, the biggest danger facing all rapidly expanding owners is that of the uncertain future of the shipping markets. Having committed tens of billions of US Dollars in the expansion and young age of its fleet, Greek owners need the support of prolonged and healthy shipping markets. A deep crisis, especially one affecting most of all the shipping sectors simultaneously, would endanger Greek shipping and its ability not only to survive but also to commit the huge capital required to continue its growth.

The two main external dangers that would affect shipping are either a global financial crisis or the growth of protectionism. The rise of populist governments across the world threatens international trade and we have already seen the effects of such rise.

The risk of a global financial collapse is always present. The extreme expansion of global debt has rendered such risk as not improbable anymore. Quantitative easing may have been popular with central bankers and politicians alike, but at some point the debt build up needs to slow down and even reverse.

Managing the global financial risks will be a huge challenge ahead for all central banks and nations.

Greek shipping may well suffer more than most under such conditions. This threat raises two issues. The first is the need to build up liquidity and reserves sufficient to address the effects of a financial meltdown. Such a conservative approach may well slow Greek shipping’s growth over the next years. There are already signs that Greek owners have begun to slow down their investments as witnessed by a smaller Greek newbuilding orderbook. The second issue is one of diversification. Greek owners have tended to overcommit in one sector (i.e. shipping) and this poses huge questions should the shipping markets falter. Diversification into other countercyclical investments may reduce the intrinsic risk faced by Greek owners. Once again, this may result in a slowdown of the growth of Greek shipping.

To conclude, therefore, Greek shipping continues to meet the challenges of competitiveness and commitment. It now faces, though, higher risks related to protectionism and unstable financial markets, which may render a further rapid expansion as unduly aggressive. Meeting such challenges may well shape Greek shipping in the next decade and may affect its ability to remain the number 1 global shipping provider.

* Head Petrofin Research ©